Why Every Small Business Needs a Backup Plan

Your Small Business Backup Plan, Why You Need One

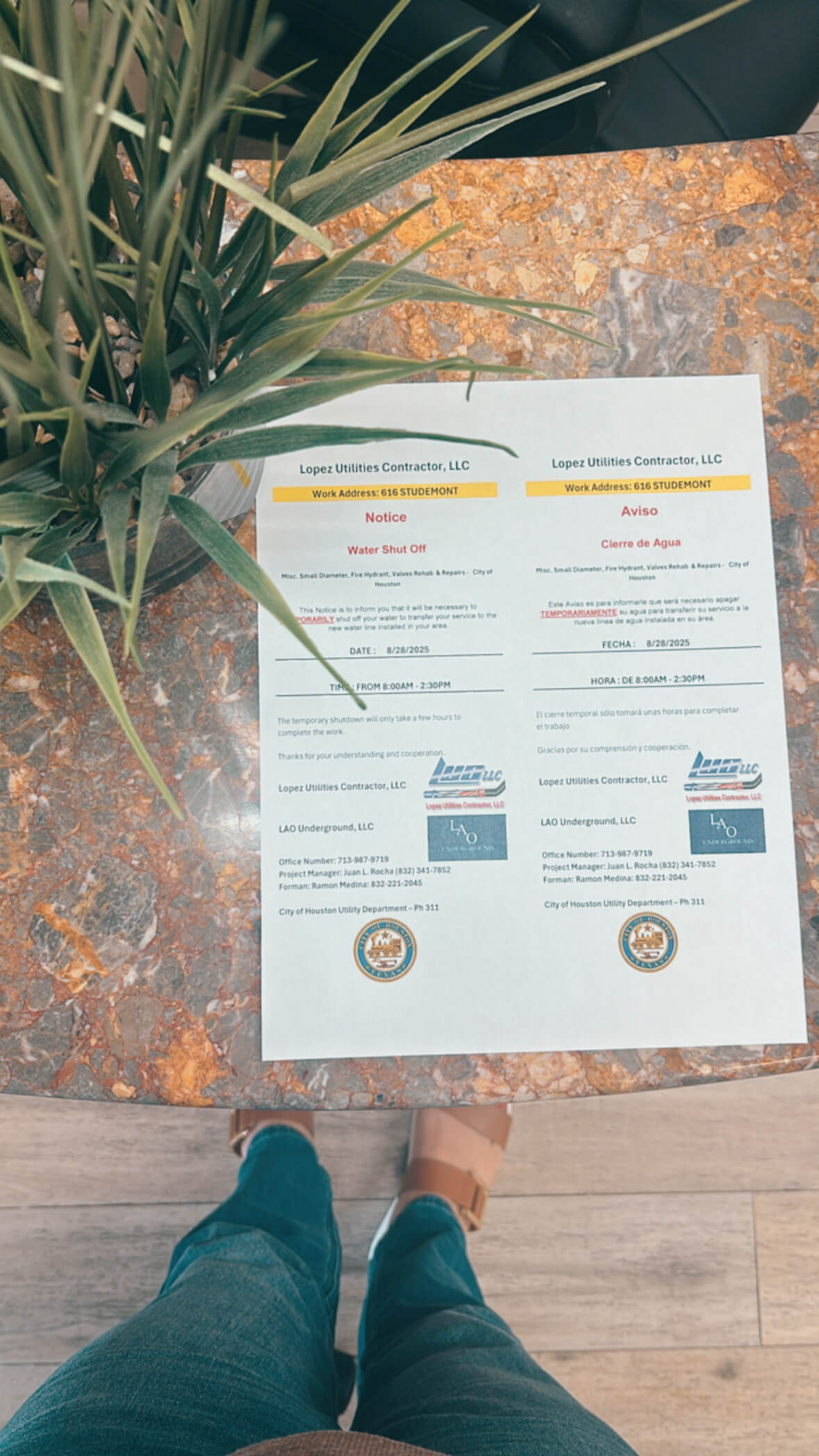

Last week, I was at my favorite local nail salon in Houston when the scariest person in the world walked in, a man in a construction safety vest. He was not there for a pedicure. He carried a piece of paper from the City of Houston notifying the owner, Tran, that water would be shut off in the area the next day. That moment reminded me why a small business backup plan is not optional. It is essential for survival.

If you are a small business owner, you know that moment of panic.

- Did I forget to pay a utility bill?

- Wait! Isn’t the bill included in my rent?

- Am I about to get shut down over a violation I did not even know existed?

As Tran read the notice, I could see her heart sink. The entire salon was full of clients, our feet submerged in warm water, yet the next day’s schedule flashed before her eyes. Dozens of appointments, potentially gone.

I suggested a quick Plan B, a run to Home Depot for five gallon water jugs. Not perfect, but enough to keep the salon operational and avoid cancellations. She smiled with relief. Sometimes the smallest backup plan saves the day.

That moment reinforced a simple truth. Every owner needs a Plan B, and often a Plan C. Here are three non negotiables.

1. Emergency Cash or Access to Credit

Every book and banker will tell you to keep three months of operating expenses in cash. If you are a small business owner, you have probably rolled your eyes at that advice more than once. For many, it feels unattainable, like advice written for companies with outside investors or corporate safety nets.

Here is the truth. Whether or not three months of cash feels realistic, you must have access to liquidity when the unexpected strikes. That is where strategy comes in.

Start with your relationship bank. Establish a business line of credit before you need it. Banks lend to businesses that do not look desperate, so apply when times are good, not when you are scrambling.

I am also a proponent of business credit cards, not just as a stopgap, but as a strategic tool. When used wisely, they do three things for you.

- Build your business creditworthiness. Consistent, responsible use creates a track record with lenders that will serve you for years.

- Provide immediate access to capital. If the AC fails in August, or a key supplier requires upfront payment, you have instant liquidity.

- Reward the owner. Points, cash back, or travel miles become assets you can reinvest into the business, or use to offset the costs you shoulder as an owner.

Think of credit cards as an emergency parachute, and a performance booster. Access to capital is what keeps your doors open when Plan A gets derailed.

Take it from me. This is not theory. My business is currently up 46% year over year, and part of that growth comes from financial fluency. I do not view credit as a liability. I view it as a tool. A well managed tool that has allowed me to scale, seize opportunities, and keep momentum when the unexpected happens.

2. A Full Bench of Employees

Here is the hard truth. If you are the only person who knows how to handle payroll, train new clients, or manage inventory, you do not just own a business. You own a ticking time bomb.

One sick day, one family emergency, one burned out key employee, and you can be in free fall. Clients do not care if you are short staffed. They care whether the experience they came for meets expectations.

The businesses that thrive train for redundancy. Document systems. Cross train staff. Build what I call a full bench. Just like a sports team, you do not want to be caught with no subs when a starter goes down.

The win is two fold. Redundancy protects the business, and it develops your people. Each time you give someone a new responsibility, you invest in their growth, not just cover your bases. You create leaders, not placeholders.

I have seen it firsthand in my company. Because we build depth, I do not panic when someone needs to step away. Another employee steps up. That kind of culture keeps talent loyal, and clients confident.

3. Technology Redundancy, Protect Your Digital Lifeline

Many owners treat technology like an afterthought. In reality, it can be a single point of failure.

What happens if your point of sale system crashes on a Saturday? If your booking platform goes offline, how do clients reserve a spot? If your Instagram account is hacked, how do you tell your community where to find you?

Technology should amplify your business, not hold it hostage. Build redundancy.

- Payments. Maintain a backup method, such as a mobile card reader, an alternate processor, or a direct pay option, so sales continue if your main system hiccups.

- Marketing and communication. Own your client list. Social platforms can disappear without warning, but an email list keeps your message resilient.

- Data and files. Store critical assets in the cloud with multifactor authentication. One hardware failure should not erase your history.

Think of technology like plumbing in that nail salon. Most days it flows quietly in the background. The second it is gone, your entire operation stops. If you are serious about your livelihood, do not leave your digital backbone unprotected.

Build Your Small Business Backup Plan Today

Start simple. Confirm your line of credit. Add a second payment pathway. Choose one critical process to document this week. Invite one team member to shadow you in a task that only you can do. Small steps, big stability.

We do not choose when the person in the safety vest walks through the door. We do choose how prepared we are. A small business backup plan built on emergency liquidity, a strong bench of employees, and technology redundancy is not a luxury. It is a lifeline. Owners who succeed long term are not just great at Plan A. They already built Plan B.